By Dennis Karpenko, CFA®

Markets continued their rebound in May, building on an upward climb from the recent pullback in early April, amid improving consumer sentiment and easing trade tensions. U.S. trade negotiations with the European Union (EU) have progressed, delays to tariff hikes, and more global trade stability have largely supported a broad-based increase in equities. Overall, the quick recovery provided a perfect example of why “weathering the storm” and remaining invested in the market is the best course of action for long-term investors.

Equities

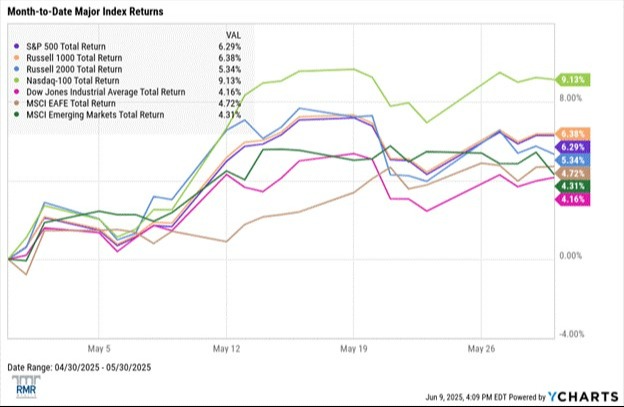

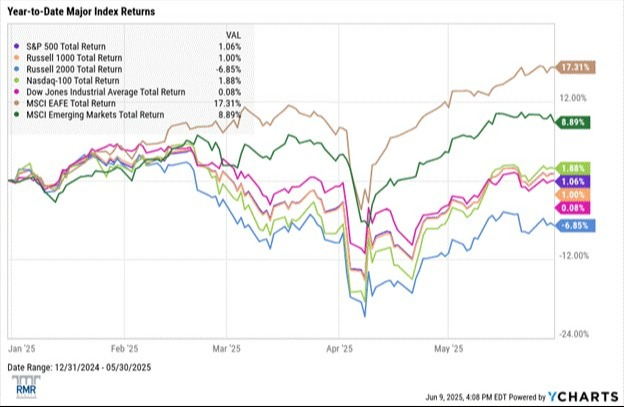

The S&P 500 posted a 6.3% return in the month of May, pushing the index back into positive territory for 2025. Technology was the strongest performing sector, posting a near 10% return in the month of May; other sensitive sectors like Industrials and Energy also returned a positive print, underpinning the widespread nature of the market’s bounce back.

Aside from sector performance, the market rise was due in part to a very healthy first-quarter earnings season. Within the S&P 500, over 70% of companies reported positive earnings surprises, and over half had favorable revenue expectations.

International equity also reflected a positive month with both the MSCI EAFE and the MSCI Emerging Markets indexes returning over 4% in the month of May. These indexes have thus far had a very healthy year, outperforming domestic indices in the wake of a turbulent Spring in U.S. markets.

Fixed Income

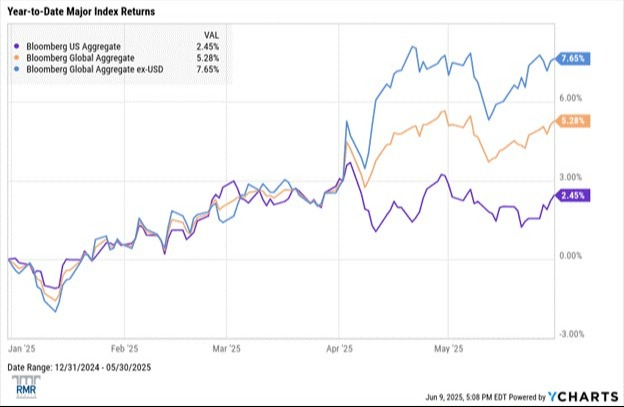

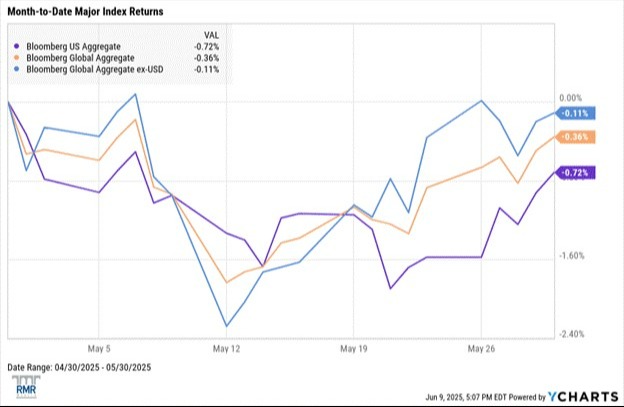

Unlike equities, U.S. fixed income has had a relatively muted month. A flurry of competing factors, such as inflation, slowing growth figures, and a downgrade in the U.S. debt rating, resulted in uncertainty, with yields ultimately moving higher. Moody’s first graded the U.S. debt with its highest rating in 1919 and was the last of the three major credit rating agencies to downgrade it when it did so in the middle of May. This adjustment brings the U.S. from Aaa (the highest rating) to Aa1, the second highest on a scale of 21 different ratings.

High-yield outperformed investment-grade debt and sovereign debt, indicating an improved tolerance for risk. Sovereign yields (bonds issued by governments) largely fell into two groups depending on the health of the underlying country’s fiscal position; countries with a weakening fiscal position (such as the U.S. and Japan) underperformed, while countries with respectively stronger fiscal positions performed better.

Economic Recap

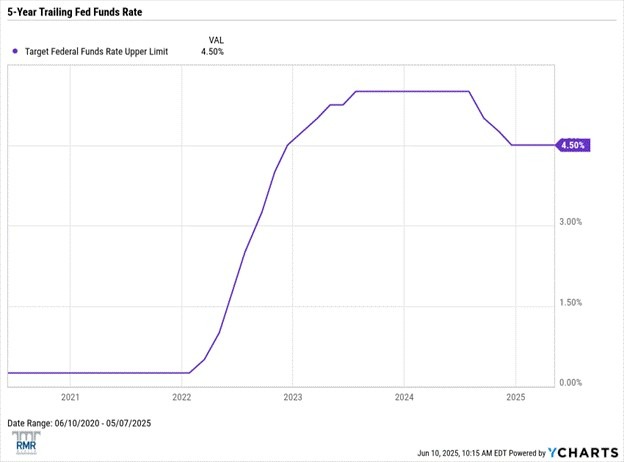

The Federal Reserve (Fed) held its target federal funds rate steady in the 4.25%-4.50% range during their May meeting. There have been no cuts to rates so far in 2025, despite estimates of up to 3-4 cuts initially heading into 2025. Their official statement notes unemployment and sticky inflation since March as primary concerns and justifications to keep rates steady at this time.

Other notable economic figures:

- U.S. Labor Force Participation Rate of 62.40% (down from 62.60% in April)

- U.S. Unemployment Rate of 4.20% (steady from April)

- U.S. Inflation Rate of 2.35% (up from 2.31% in April).