By Dennis Karpenko, CFA®

The month of August saw fairly strong returns across most major asset classes. Overall, the second quarter earnings season was positive for companies as many beat analysts’ estimates. Arguably, the most prominent economic news to come out of the month was the Federal Reserve’s annual summit for central bankers, where Fed chair Jerome Powell made statements alluding to greater odds for a rate-cut in the Fed’s forthcoming September meeting.

Equities

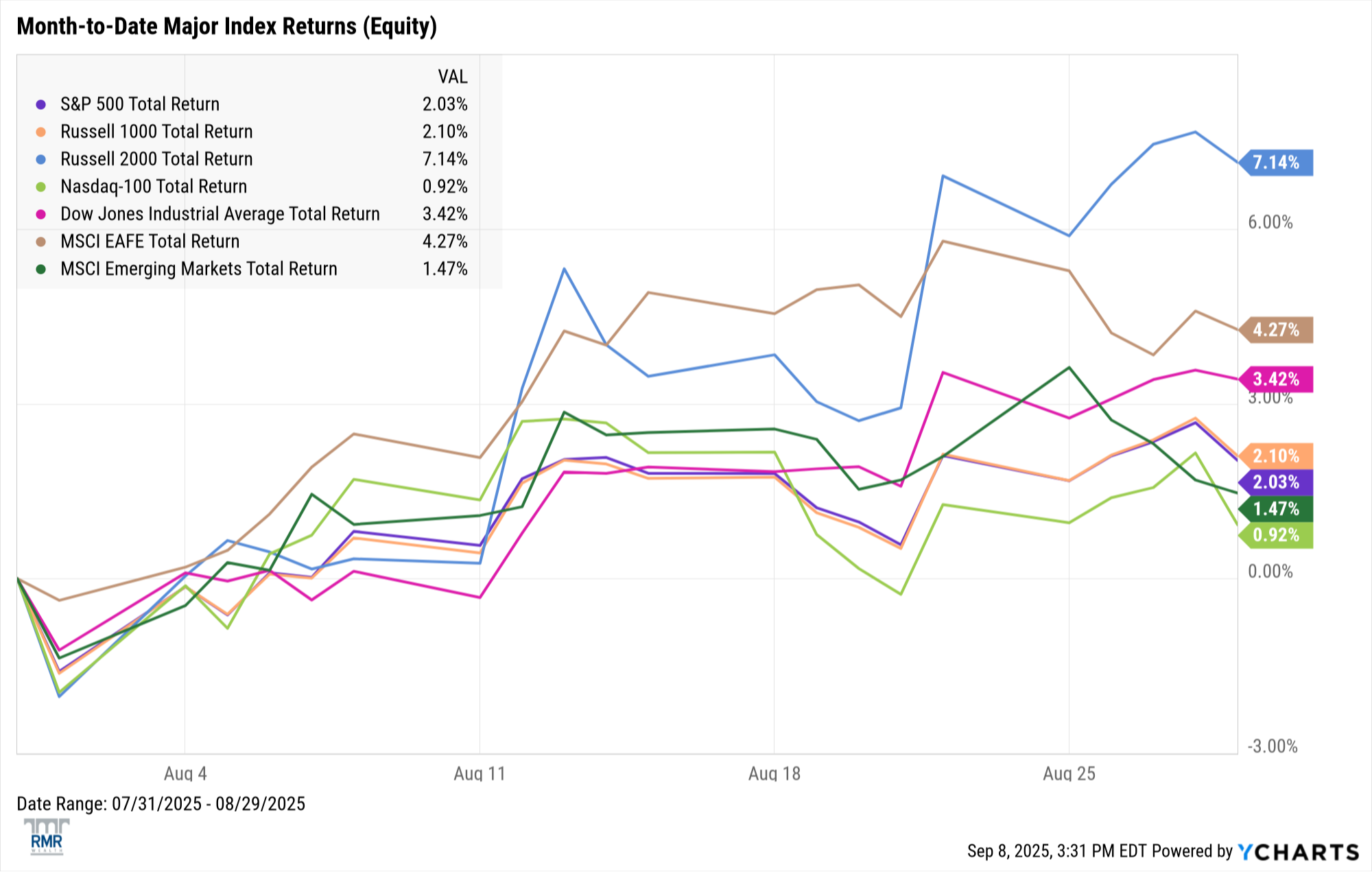

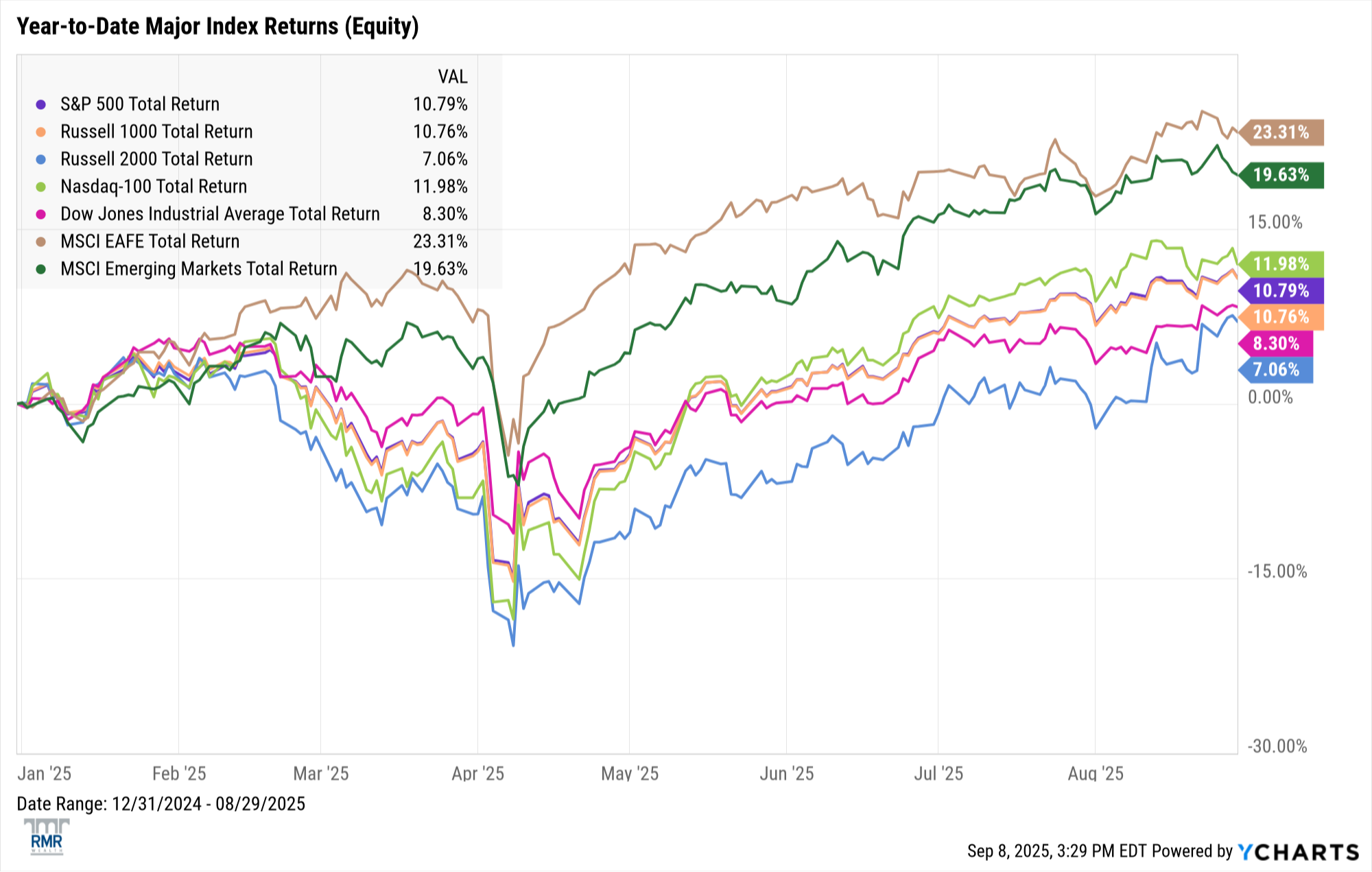

August saw another positive month for equity indexes as the S&P 500 printed another month over 2% in total returns; the index is now up just over 10.5% year-to-date. The biggest jump, however, came in the small-capitalization space as the Russell 2000 returned over 7% for the month. Although the index is up just over 7% for the year, rate-cut optimism has pushed many smaller companies higher.

International indexes continue to perform strongly. Both developed and emerging markets international indexes are up over 19% year-to-date, a stark contrast to recent years, where domestic equities have largely outperformed. Many sectors were positive over the period as well. Healthcare, the worst-performing sector year-to-date, led the month with over a 5% and is now positive in 2025.

Fixed Income

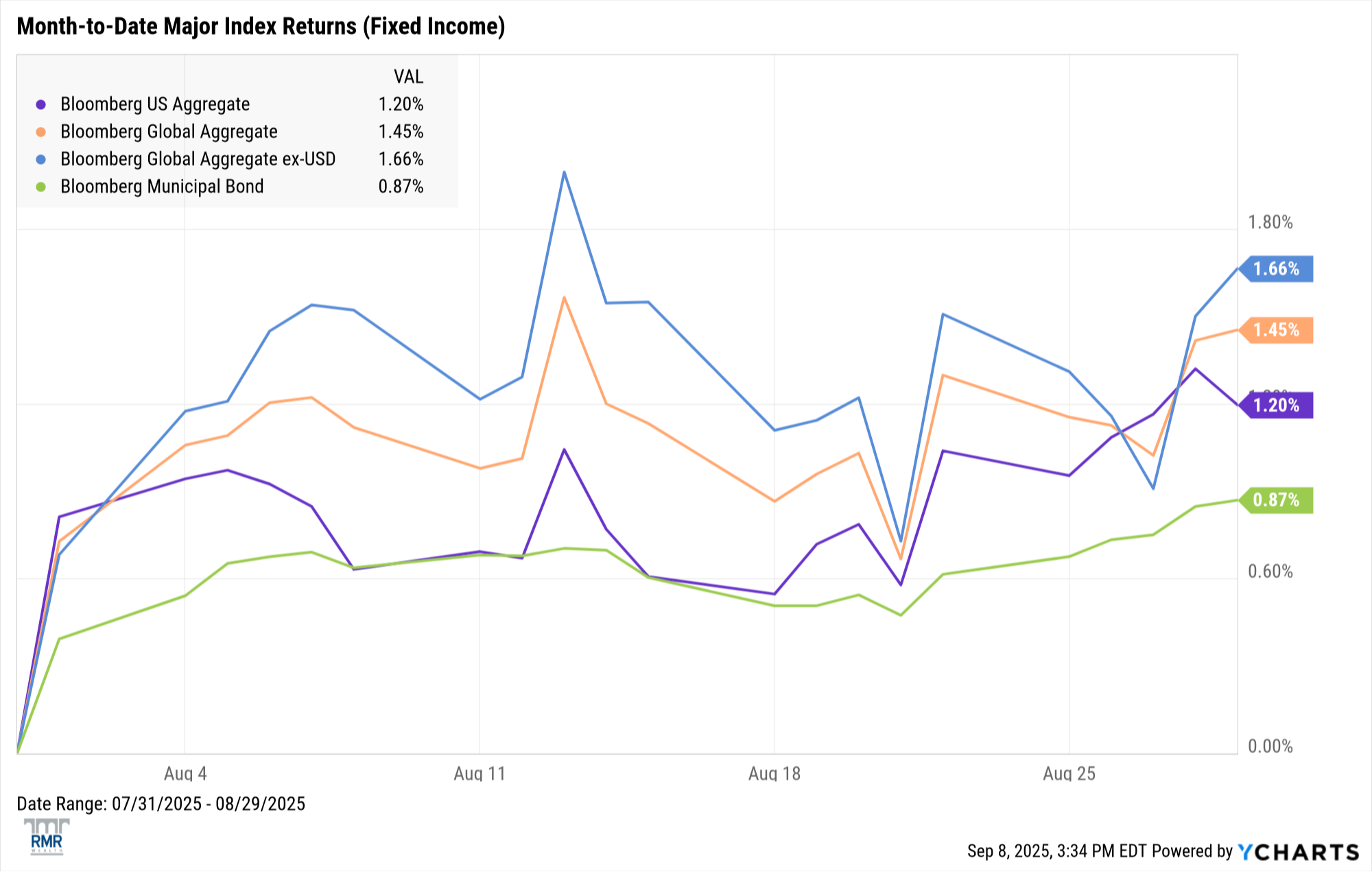

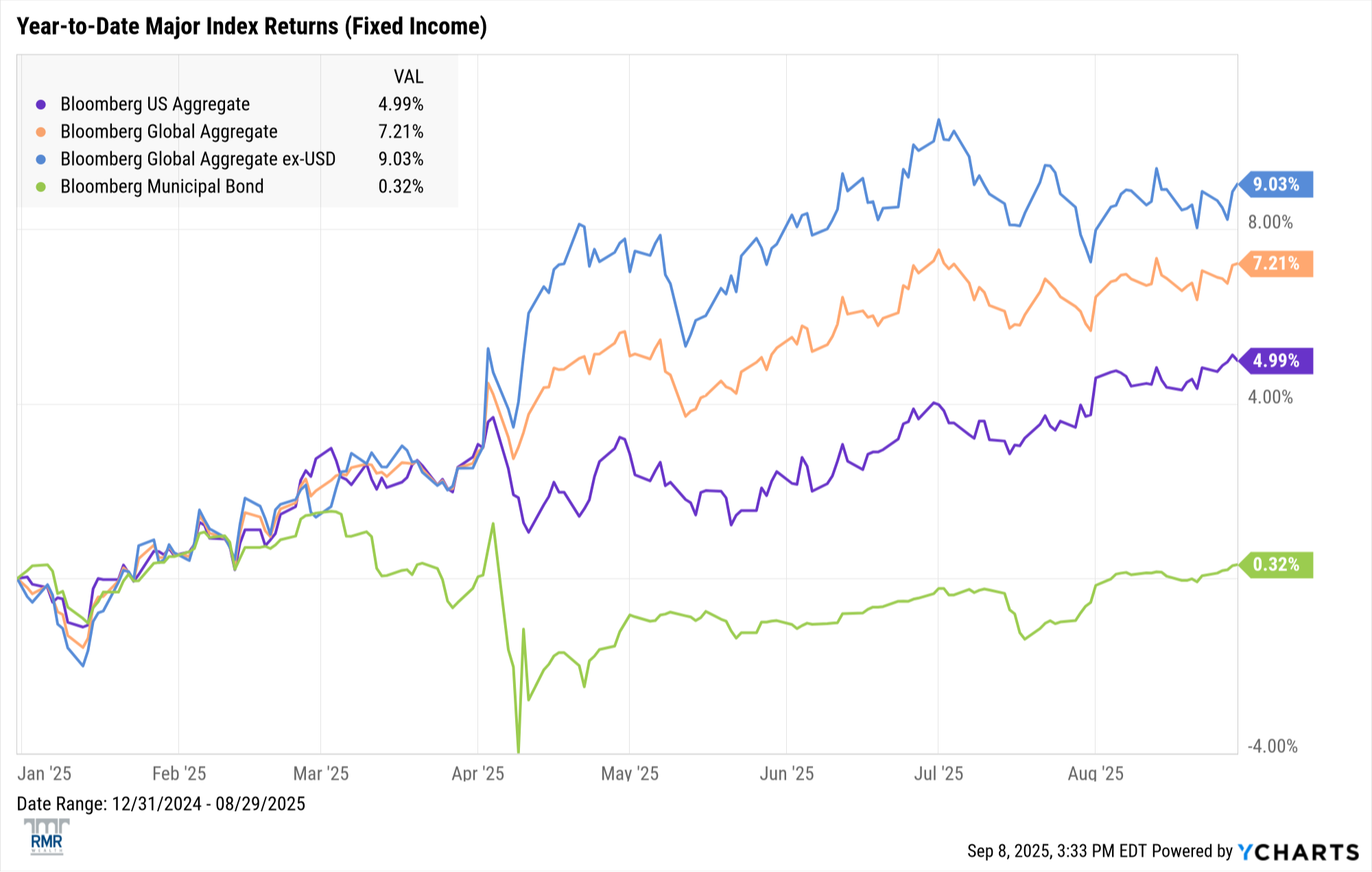

Investment-grade spreads continued to tighten across both Europe and the United States, leading to gains in U.S. and global aggregate indexes. Expectations for Fed rate cuts helped contribute to longer-duration investment-grade bonds. This news has also led to a curve steepening for treasury bonds as short-term rates fell, while longer-term yields commensurately rose.

Separately, the Bloomberg Municipal Bond Index saw a nearly 1% return on the month, pushing the index into positive territory for the first time since early April.

Economic Recap

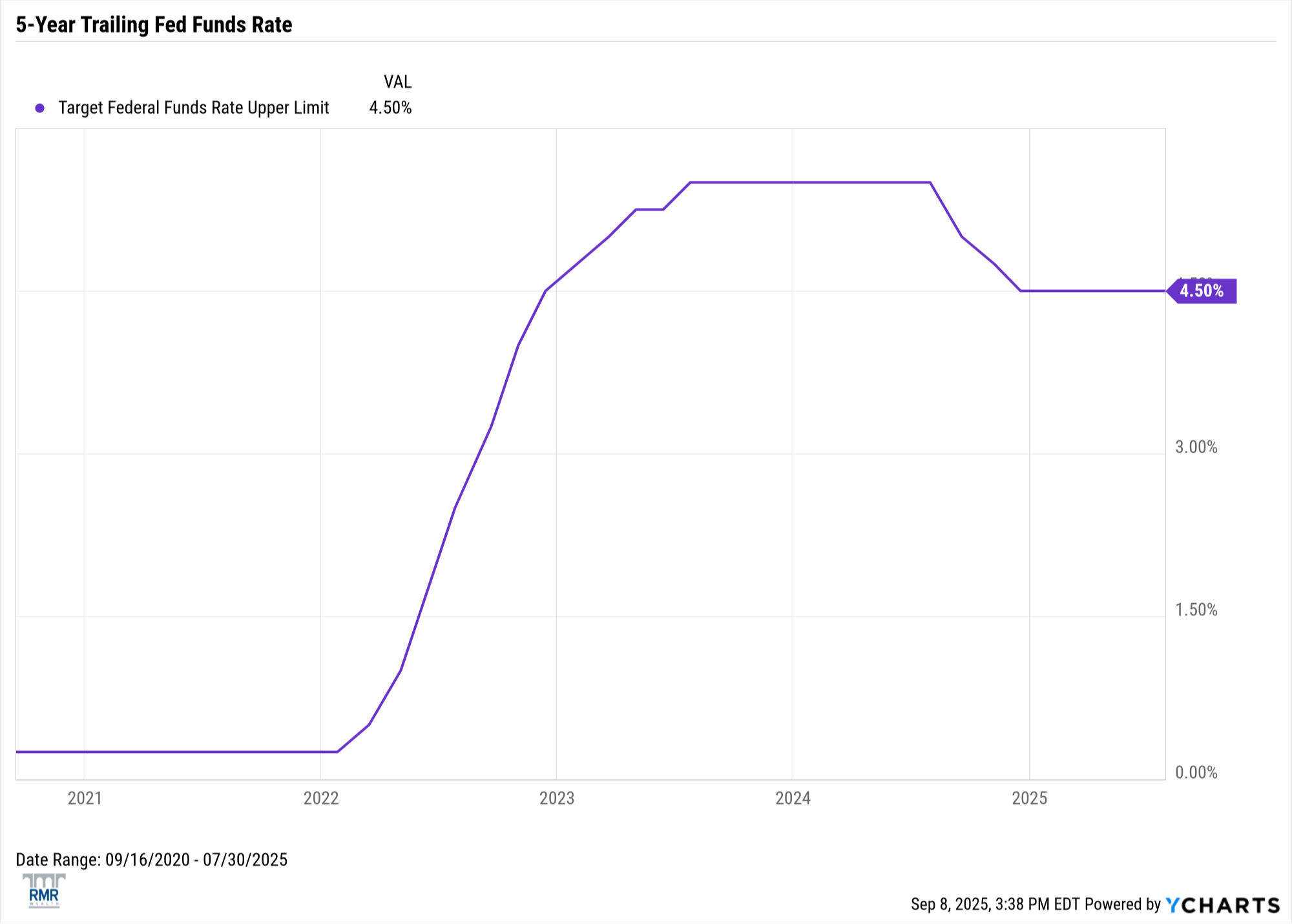

The Federal Reserve’s next interest rate meeting is slated to occur on September 17th with expectations pointing to a small cut in rates on the heels of Fed Chair Jerome Powell’s comments at August’s Jackson Hole Economic Policy Symposium. Despite negative U.S. labor market news, inflation largely remains under control and global activity remains resilient.

- U.S. Labor Force Participation Rate of 62.30% (up from 62.20% in July)

- U.S. Unemployment Rate of 4.30% (up from 4.20% in July)

- U.S. Inflation Rate of 2.92% (up from 2.70% in July)

Read the Next Article

Disclosures

Investing involves risks, and investment decisions should be based on your own goals, time horizon, and tolerance for risk. The return and principal value of investments will fluctuate as market conditions change. When sold, investments may be worth more or less than their original cost.

The forecasts or forward-looking statements are based on assumptions, may not materialize, and are subject to revision without notice.

The market indexes discussed are unmanaged and generally considered representative of their respective markets. Index performance is not indicative of the past performance of a particular investment. Indexes do not incur management fees, costs, and expenses. Individuals cannot directly invest in unmanaged indexes. Past performance does not guarantee future results.

U.S. Treasury Notes are guaranteed by the federal government as to the timely payment of principal and interest. However, if you sell a Treasury Note prior to maturity, it may be worth more or less than the original price paid. Fixed income investments are subject to various risks, including changes in interest rates, credit quality, inflation risk, market valuations, prepayments, corporate events, tax ramifications and other factors.

International investments carry additional risks, which include differences in financial reporting standards, currency exchange rates, political risks unique to a specific country, foreign taxes and regulations, and the potential for illiquid markets. These factors may result in greater share price volatility.

Please consult your financial professional for additional information.

This content is developed from sources believed to be providing accurate information. The information in this material is not intended as tax or legal advice. Please consult legal or tax professionals for specific information regarding your individual situation.