The IRS has announced the 2025 dollar limits and retirement plan thresholds, reflecting the latest cost-of-living adjustments.

The 2025 limits reflect some of the smallest year-over-year increases in recent years. Of the limits shown in the table below, the key employee limit is the largest percent increase, followed by the amount used to determine highly compensated employees. No catch-up contribution limits were adjusted this year but changes under the SECURE 2.0 Act of 2022 that will take effect in 2025 (described further below) will potentially increase the limitations for catch-up contributions for certain individuals, between ages 60 to 63, eligible to make these contributions.

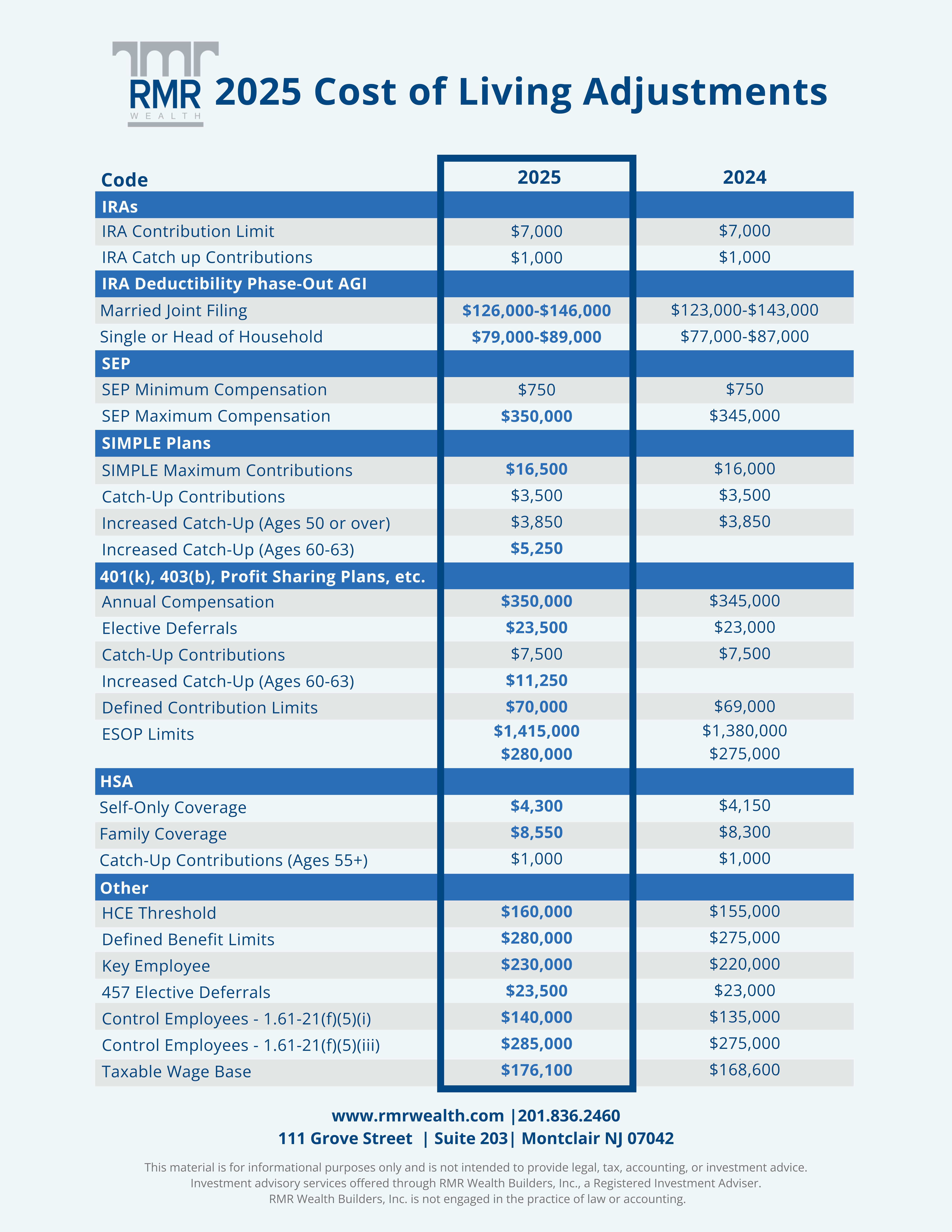

Important Highlights

- Catch-up Contributions: Catch-up contributions are permitted to be made for participants beginning in the year in which they turn age 50. For 2025, the limit on catch-up contributions is $7,500, except in the case of Savings Incentive Match Plan for Employees of Small Employers (SIMPLE) plans for which the limit is $3,500 (both unchanged from 2024).

- 60 to 63 Super Catch-up Contributions: Due to changes under the Act, beginning in 2025, the catch-up limit for most retirement plans is increased to $11,250 for individuals turning 60, 61, 62, and 63 during 2025. For SIMPLE plans, the limit is increased to $5,250. These increased amounts are indexed for inflation after 2025. These increased limits will apply to most workplace retirement accounts, including 401(k)s, 403(b)s, and government TSPs. While IRA limits remain at $7,000 ($8,000 if you're 50+), this extra room in workplace accounts opens up new possibilities for your retirement strategy. This means if you're between 60 and 63, you could contribute up to $34,750 in 2025. It's important to note that the 60 to 63 super catch-up is optional for employers and typically requires a plan amendment. Employers will need to opt in to offer the super catch-up provision.

- IRA Phase-outs: Income phase-out ranges for various IRA purposes increased from between $77,000 and $87,000 to between $79,000 and $89,000 for single and head-of-household taxpayers. Similar incremental changes were made to the limits for married filing jointly and married filing separately taxpayers.

- IRA Catch-up Contribution Limit: The IRA catch-up contribution limit for individuals aged 50 and over was amended under the Act to include an annual cost of living adjustment but remains $1,000 for 2025.

- SIMPLE Plans Contribution Limit: The amount that may be contributed to SIMPLE retirement plans is increased to $16,500 from $16,000. Due to changes made under the Act, participants in certain SIMPLE 401(k) and SIMPLE IRA plans can take advantage of an increased deferral limit of $17,600 and an increased catch-up limit of $3,850 (both unchanged from 2024) if their employer meets specific conditions.

Click Here to Download the 2025 Cost of Living Adjustments